A tale of two states

Over six months ago, as the COVID-19 pandemic’s first year drew to a close, this column foresaw a ‘two speed’ recovery of domestic and international air travel (see December 15, 2020 column here).

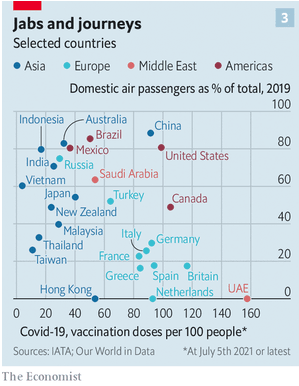

Back in December 2020, with vaccines due to arrive in a few months there was a good chance that some passenger markets, especially with those with strong domestic networks, would rebound strongly in the coming year. But an accurate forecast was impossible. Freight remained the only sustained bright spot (Cargo the last hope) in an otherwise gloomy outlook for 2021. Today, as vaccines are being produced in greater quantities we see some recovery, but it is a phased one that largely appears to depend on the success of mass vaccination programs and restriction-free domestic travel. The chart from the The Economist magazine clearly shows the relationship between sufficient vaccinations the size of a nation’s domestic travel market.

A perennially bad investment

As this column has mentioned previously, the airline business is potentially disastrous for investors. Ranked by declared profits and ROI (return on investment), airlines were always a poor investment for capital. The industry’s main voice, the International Air Travel Association (IATA), estimates that fewer than half the world’s airlines earned more than their cost of capital in the 2008-2018 period. The pandemic exacerbated this poor performance, with most airlines now reliant on state aid for their continuing existence, to the extent of an enormous USD 225 billion globally, according to IATA estimates.

While bailouts have kept many airlines operating, it is now becoming obvious that the effects have been mixed at best. As the vaccine rollout has amply demonstrated, those nations blessed with good governance and deep pockets have been able to begin their recovery, and airlines based in many of those places are showing signs of revival. The US airlines, who collectively received over USD 54 billion in government payroll support, have now begun paying it back as domestic traffic recovers strongly.

Domestic first

China, where the COVID-19 pandemic was first identified, has handled it with commendable (if harsh) efficiency. Despite extreme lockdown measures which most other nations cannot implement, the virus has re-emerged, most recently in the Guangzhou region. But despite these setbacks, Chinese domestic aviation appears to have returned to parity with, or even exceeding, 2019 levels. The closure of the country’s international borders has benefitted China’s Big Three, who flew many loss-making international routes only because they were required to for political reasons. Air China, China Southern and China Eastern are joined by privately-owned Spring Air in an effective oligopoly of the market, as Hainan Airlines (the pretender to the big league) suffers from a crippling debt burden.

China’s success in vaccination a significant proportion of its citizens (see chart) has no doubt contributed to this rebound.

Similarly in the USA, where a successful vaccine rollout has seemingly blunted the worst of the pandemic, the Big Three (United, American and Delta) plus domestic giant Southwest Airlines, have been reporting a resurgence in travel. These four huge airlines control about 80% of the US market, which until 2020 was the world’s largest market. That title is currently held by China due to the pandemic’s toll on US travel last year. Over 80% of passengers in the US were traveling on domestic routes in 2019, so as vaccinations continue there is little doubt that the USA will regain the top spot soon. This confidence is amply demonstrated by the announcement that United Airlines placed the largest order in the company’s history for 200 Boeing and 70 Airbus jets, though crucially these are all ‘single-aisle’ types intended for shorter routes.

Europe on the other hand is seeing a different type of recovery. There is no EU-wide vaccination program, with each country left to its own devices.The Uk has had the most widespread vaccine rollout so far, but the small domestic market in britain has meant the impact on air travel has been minimum. With ‘international’ travel within Europe subject to patchy and sometimes contradictory restrictions, it is hard to measure the actual impact on airlines. However, it appears that cash-rich Low Cost Carriers (LCCs) such as Ryanair, Wizz Air and easyJet are best positioned to recover soon. The larger European national airlines who were reliant on long-haul international traffic for a larger portion of their business, will recover more slowly. British Airways, part of the International Airlines Group, has moved quickly to slash costs and get rid of surplus aircraft. But others such as Lufthansa, Air France-KLM and Alitalia have not restructured as aggressively, and are limping by on government bailouts.

India’s domestic sector, which was not far behind the USA, China and Europe, has suffered from the pandemic’s devastating ‘second wave’ which brought India to its knees. Indigo Airlines in particular was poised for recovery late in 2020 when it appeared that Asia had weathered the pandemic relatively unscathed. That optimism proved unrealistic, and it will now be many months until an erratic vaccination program blunts the spread of infections on the sub-continent sufficiently for unrestricted domestic for travel to resume.

On the other side of the world, both Australia and New Zealand showed strong domestic travel patterns, and the ‘travel bubble’ between the two countries was progressing well. A recent surge of infections spread by inbound travellers with the ‘Delta variant’ has seen lockdowns in most of Australia’s capital cities (at this time of writing Sydney’s has been extended by another week) and inter-state border closures, resulting in a plunge in traffic.

A comprehensive shake-up may be ahead?

Is it possible that the long-term effects of the pandemic may lead to a significant, and long overdue, realigning of the entire sector? As is becoming obvious, the world’s recovery will be staggered at best. Those countries that dealt with the pandemic well or effectively achieved comprehensive vaccination rates have already started to open up. Travel from the USA to Europe is picking up strongly, and inter-European bookings for travel during the crucial summer season is surging, though it is patchy due to uncoordinated travel restrictions. The additional cost of COVID tests, running into hundreds of USD per traveller, has made it costlier still.

Asia, sadly, shows no sign of a quick recovery, with the region’s second-most populous country, Indonesia, now stumbling into a crisis which appears to be as bad as India’s. Even Thailand, Malaysia and Vietnam, which had a relatively easy ride in 2020, are seeing significant surges of the virus. Singapore has suffered recurrent lockdowns despite the region’s best vaccination program. The island-state’s flag carrier, Singapore Airlines, is joined by other Asian giants Cathay Pacific (based in Hong Kong), Dubai’s Emirates Airline and Qatar’s national airline in being essentially reliant on the whole world reopening, as they are dependent on connecting passengers to feed extended ‘hub and spoke’ systems. A patchy recovery, with some ‘spokes’ having minimal traffic, can make the whole network unprofitable.

Asia’s dinosaur state-owned national airlines are another story. Even in the peak profitable years when fuel prices (the single biggest variable cost for most airlines) were low, most of these perennial loss-makers needed state support and received it, as they were seen as a source of patriotic pride.

Obtaining and deploying effective vaccines to fully inoculate a sufficient portion of the population in order to achieve ‘herd immunity’ is seemingly the only path to pre-2020 normality. While national treasuries struggle to meet the needs of this vital program, the chances of there being enough spare cash to prop up ‘vanity airlines’ are increasingly unlikely.

Leave a Reply